This content is from:APP亚博娱乐

How Factors Can Help Reduce Risk in Corporate Bond Exposures

From the Nov 2020 BlackRock Alternatives Special Report 1

Managers of income strategies are faced with the dilemma of all-time low bond yields and dividend paying stocks exhibiting significant volatility. The questions these circumstances raise are: Do managers reduce income targets? Or take on more risk in search of yield? The answer may be neither, as this brief report explores.

1How Factor ETFs Can Help Achieve Target Income

Utilizing factors such as quality, minimum volatility, and value alongside existing equity/bond positions could help managers of income strategies maintain target income levels while seeking improved resilience.

Here’s how:

- Consider allocating to equity and bond factor ETFswith the goal of diversifying some of the unique risks associated with today’s income-seeking strategies. These can include specific sector/factor biases and idiosyncratic risks.

- BlackRock can provide customized portfolio consulting, including risk analysis, for institutional investors.

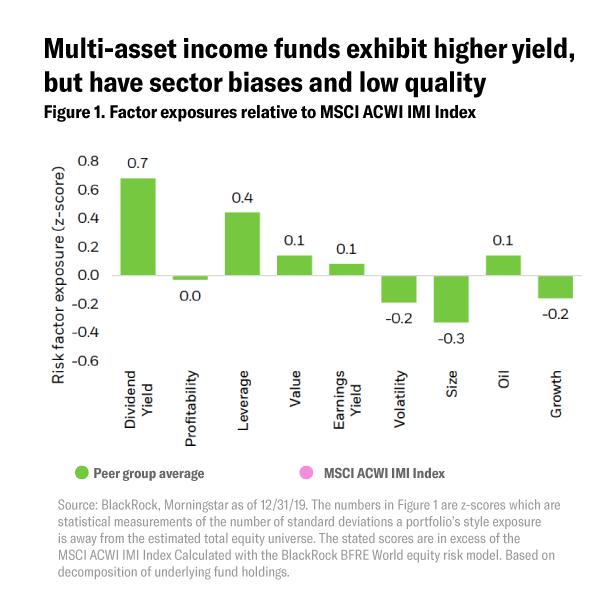

A BlackRock study of 83 multi-asset income mutual funds (“peer group”) representing over $240 billion in assets1发现了重要的部门和因素风险。

- Using a proprietary risk model, analysis of the peer group’s equity style factor exposures (see Figure 1, below) showed strong exposure to high dividend-yielding stocks, but at the cost of higher leverage and lower profitability – a negative quality bias which could drag on return. The average fund also exhibited meaningful smaller-cap, value, and anti-growth tilts.

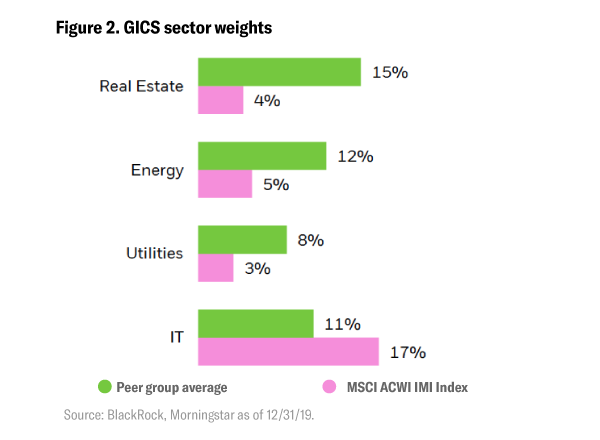

- 平均基金也显示出来large overweights to the real estate, energy, and utilities sectors(see Figure 2, below). These sectors have historically paid an attractive dividend yield but can exhibit increased sensitivity to interest rate changes and fluctuations in energy supply and demand.

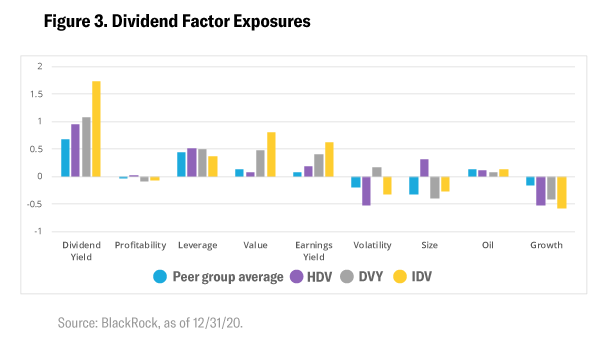

- Equity dividend ETFs (i.e., iShares Core High Dividend ETF [HDV], iShares Select Dividend ETF [DVY], iShares International Select Dividend ETF [IDV]) tend to exhibit similar directional factor exposures (see Figure 3, below).

Deeper Look

“Using a factor lens for an income portfolio may help reduce the ‘yield traps’ that can hurt the equity income investor. For example, some high yield stocks may have unsustainable payouts and high volatility. Considering the quality characteristics of a stock based on its fundamentals may help reduce volatility and ensure a sustainable payout. To this end we often find institutional and wealth investors include quality and minimum volatility factors to complement the income portfolio.”

– Mark Carver, Managing Director, Global Head of Equity Factors, MSCI

“在投资领域,我们看到两种方法investors who have largely built their portfolios stock by stock and bond by bond, and others who use managed solutions run by their larger organization. If you’re someone who builds portfolios using individual securities, factors play a role, but you’re not necessarily always considering what factor exposures arise as a by-product of your stock selection. In that case, we can help clients form a view on momentum or increased volatility. We can show them how to potentially lower their overall volatility exposure with an ETF that gives them market-like exposure without requiring them to decide on which stocks they need to buy and sell.”

– Del Stafford, Head of iShares Portfolio Consulting, BlackRock

![]()

1截至12/31/19

2How Factors Can Help Reduce Risk in Corporate Bond Exposures

Finding sufficient bond income has become harder, leading portfolio managers to take on more risk by extending duration and reducing credit quality. The average fund in the peer group allocated more than half of its fixed income sleeve/allocation to corporate bonds (see Figure 4, below), a meaningful difference from the aggregate bond benchmark.1这些企业债券分配中包含的投资级和高收益债券可能具有较低的质量,以实现收入目标,这增加了投资组合的风险。

Fixed income factors like quality and value can offer risk diversification and help investors manage downside risk while maintaining similar or higher levels of yield. iShares Investment Grade Bond Factor ETF (IGEB) and iShares High Yield Bond Factor ETF (HYDB) seek to target these two factors in the corporate bond space.

质量因素筛选债券具有更高的默认概率,将投资组合倾斜,以具有更高默认调整的差价的公司债券。这种较低的默认概率可以伴随着较低的产量。这就是为什么质量因子互补的值因素,这是债券相对于他们的基本面便宜的界面。

The aforementioned iShares ETFs exhibit lower probability of default and similar or higher yield (see Figure 5, below) than their traditional counterparts, helping managers continue to allocate to IG and HY corporate bonds in pursuit of higher income with potentially less risk.

Deeper Look

“随着因素ETF,股票的质量和最小波动的巨大范围,固定收入的质量和价值,以帮助满足收入需求,随着额外保护的多样化和额外保护。

– Andrew Ang, Head of Factor Investment Strategies, BlackRock

“因素行为有助于客户了解资产在科夫迪造成的经济不确定性期间如何定价。结果是更多客户在系统地测量其股票计划中的因子风险,以更好地了解其风险暴露,并重新定位投资组合以表达投资意见。大流行引起的不确定性使得评估公司基本面难以加上美国股票的高浓度,有利于2020年的大部分势头这样的技术因素。但是,客户要求提供像价值等的亲周期性因素可能会加强2020年市场恢复岩体变成了经济复苏。“

– Mark Carver, Managing Director, Global Head of Equity Factors, MSCI

![]()

1基准是Bloomberg Barclays美国汇总债券指数。

3A Case Study of Factor-Aware Income Generation

在Covid-19危机和随后的股权波动危机的后果,企业债券降级和记录低利率,许多多资产收入组合管理人员正在重新评估如何减轻寻求产量的风险。

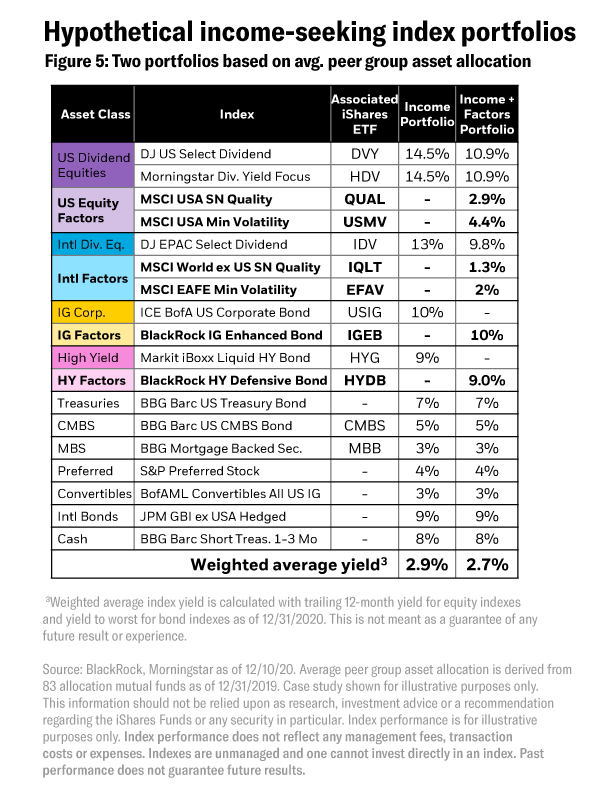

Deriving an assumed global multi-asset allocation from the peer group average, two hypothetical index-based portfolios were constructed.

- Income:The asset allocation is populated with dividend-focused equity and broad-market fixed income indexes. This represents a typical income-seeking multi-asset portfolio.

- Income + Factors:Seeks to enhance the Income portfolio by allocating 25% of equities to factor indexes and fully replacing traditional corporate bond indexes with factor-based indexes.

收入+因素产品组合对因素指标进行了小分配:

- 多元化因素和行业偏见

- 保持类似的产量水平

- 提高风险调整的性能

The inclusion of factor indexes in the Income + Factors portfolio would have diversified factor exposures, making the portfolio less reliant on value-oriented factors (see Figure 7, below). The quality factor would have been improved through higher profitability and lower leverage attributes, and the portfolio would have had more exposure to low-volatility stocks. Upgraded quality and low volatility exposure can potentially improve portfolio resilience during selloffs. Growth exposure would have become less negative, and oil would also have moved closer to that of the global benchmark.

The weighted average yield (above) shows that allocating a portion of the portfolio to factor-targeting strategies may maintain a similar level of yield.

Deeper Look

“当多资产策略中有汇集资金时,通常会有如此多的多样化,它看起来像索引 - 没有显着的主动赌注。个人积极管理人员正在活跃,但它们的职位降低了投资组合的总体主动风险,而且表现优于优势的机会。正如他们开始使用因素的那样,它们可以从目前的积极策略中区分曝光。因此,如果他们愿意将分配给一些积极的战略并使用因素ETF,他们可以增加他们的积极风险水平及其优于优势的机会。投资者和管理人员往往没有概念化这一点,因为ETF有时被视为广基指标的车辆。“–Del Standord,Head of iShares Portfolio Consulting, BlackRock

“One area that hasn’t been widely considered by income-seeking investors is to use factor strategies and factor ETFs to complement traditional sources of income. Using factor ETFs can lead to a more robustly constructed portfolio, and in some cases, even greater income as measured by dividend yields or cashflow payouts. In the first half of 2020 we saw very large drawdowns to traditional multi-asset income funds because they have large sector overweights, in particular to the real estate, energy, and utility sectors. Those sectors traditionally offer high yields, but they have potentially large sensitivities to changes in interest rates and economic growth, and to potential policy shocks – three things we had in abundance in early 2020. Those large sector overweights potentially drive higher volatility and risk, and factor ETFs can help diversify that risk while helping investors manage the downside and maintain similar or higher levels of yield. We can do that in both equities and fixed income.”–Andrew Ang,Factor投资策略,Blackrock

FOR INSTITUTIONAL USE ONLY - NOT FOR PUBLIC DISTRIBUTION

在投资前仔细考虑资金的投资目标,危险因素和费用和费用。可以通过访问www.ishares.com或www.blackRock.com,在资金招股说明书中或其他信息中找到这些信息,或者,如果可用,则可以通过访问www.ishares.com或www.blackrock.com获得。投资前仔细阅读招股说明书。

Investing involves risk, including possible loss of principal.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

There can be no assurance that performance will be enhanced or risk will be reduced for funds that seek to provide exposure to certain quantitative investment characteristics ("factors"). Exposure to such investment factors may detract from performance in some market environments, perhaps for extended periods. In such circumstances, a fund may seek to maintain exposure to the targeted investment factors and not adjust to target different factors, which could result in losses.

讨论的策略严格用于说明和教育目的,并非推荐,要约或征求购买或销售任何证券或采用任何投资策略。无法保证所讨论的任何策略都会有效。提出的信息不考虑委员会,税收影响或其他交易成本,这可能会影响特定战略或投资决策的经济后果。

由Blackrock Investments,LLC,成员Finra准备。

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by MSCI Inc., nor does this company make any representation regarding the advisability of investing in the Funds. BlackRock is not affiliated with MSCI Inc.

©2020 BlackRock, Inc. All rights reserved.iSHARES和BLACKROCK是BlackRock,Inc。的商标,或者在美国和其他地方的子公司的商标。所有其他商标都是其各自所有者的财产。

iCRMH0221U/S-1458009